Retirement withdrawal strategies are methods used to turn your savings into a steady income after you stop working. This article explains how spending changes across different stages of retirement and breaks down key strategies like the 4% rule, bucket, dynamic, and annuity approaches. It also shows how to choose the right plan based on your needs and how a three-phase strategy can help your money last longer.

You spend years building your savings, step by step, with a clear goal in mind. Retirement feels like the point where all that effort finally starts to pay off. But once that phase begins, a new question takes over. How do you start using that money without running out too soon?

Taking money out sounds simple, but every choice carries weight. Withdraw too much, and your funds may not last. Withdraw too little, and you might limit the life you worked hard to create. Timing, order, and consistency all begin to matter in ways they did not before.

That is where retirement withdrawal strategies come into focus. They shape how you turn your savings into a steady income, balance risk with stability, and make sure your money supports you through every stage of retirement.

How does retirement spending change over time?

Spending in retirement does not stay fixed. It shifts as your lifestyle and health change. Most people follow a simple pattern over time. Understanding this pattern helps shape smarter retirement withdrawal strategies. You spend more early, less in the middle, and more again later.

- In the early years, spending is high. You travel, explore hobbies, and enjoy free time. Big plans that were delayed now take priority. Daily costs also rise with an active lifestyle.

- In the middle years, spending slows down. Travel reduces, and routines become simple. You stay home more and avoid large purchases. Expenses feel steady and easier to manage.

- The later years see costs rising again. Health care becomes a major expense. You may need support at home or assisted care. Medical needs can quickly increase your spending.

This pattern is often called go-go, slow go, and no-go years. It gives a clear way to plan withdrawals. Your income should adjust as your spending changes.

What are some age-based withdrawal strategies?

Different retirement withdrawal strategies follow clear rules. Each one works best at a certain stage of life. The goal is to match your income with your needs while protecting your savings.

1. The 4% Rule

Ideal age range: 60 to 75

Financial planner William Bengen introduced the 4% rule in the 1990s in a paper he published in the Journal of Financial Planning. He studied past market data to find a safe withdrawal rate. The idea is simple. You withdraw 4 % of your total savings in the first year. After that, you increase the amount each year to match inflation.

For example, if you have ₹1 crore, you withdraw ₹4 lakh in the first year. If inflation rises by 5 % next year, you will increase your withdrawal to ₹4.2 lakh. This gives you a steady income that keeps up with rising costs.

This strategy works well for people who want a predictable income. It reduces the need to make constant decisions. It also helps you plan your lifestyle with more confidence.

Risks:

- Market falls early can reduce your portfolio fast

- Fixed withdrawals may not match changing needs

- It may not last if you live longer than expected

2. Fixed Percentage Strategy

Ideal age range: 65 to 80

This method adjusts your withdrawals based on your portfolio value. Among flexible retirement withdrawal strategies, this one responds directly to market changes. You choose a fixed rate, such as 3% or 5%. Each year, you withdraw that %age from your current balance.

For example, if your portfolio is ₹1 crore and you use a 4 % rate, you withdraw ₹4 lakh. If the market drops and your balance becomes ₹90 lakh, your next withdrawal becomes ₹3.6 lakh. If markets rise, your income also increases.

This strategy protects your savings during bad markets. You never withdraw too much because the amount adjusts automatically. It also works well for people who can manage flexible spending.

Risks:

- Income can fall during market downturns

- Hard to manage fixed expenses like rent or bills

- No clear income stability

3. Bucket Strategy

Ideal age range: 60 to 80

This method divides your money into separate buckets based on time. The first bucket holds cash for 2 to 3 years of expenses. The second bucket holds bonds for medium-term needs. The third bucket holds stocks for long-term growth.

You withdraw money from the first bucket for daily expenses. When it runs low, you refill it from the second bucket. When markets perform well, you move gains from stocks into safer buckets.

This approach gives both safety and growth. You avoid selling stocks during market crashes because your short-term needs are already covered. It also gives peace of mind during volatile periods.

Risks:

- Needs regular monitoring and rebalancing

- Poor planning can empty short-term funds early

- Emotional decisions can affect timing

4. Dynamic Withdrawal Strategy

Ideal age range: 60 to 75

This method adjusts your withdrawals based on market conditions. You withdraw more when markets perform well and reduce spending when they fall. Some people use rules like cutting spending by 10 % after a bad year.

For example, if your portfolio grows by 10 %, you may increase your withdrawal slightly. If it drops, you reduce your spending for that year. This keeps your portfolio stable over time.

This strategy works well for people who can adapt their lifestyle. It protects your savings from large market losses. It also allows higher withdrawals during strong years.

Risks:

- Income becomes unpredictable

- Requires discipline to cut spending

- Can feel stressed during downturns

5. Annuit- Based Strategy

Ideal age range: 70 and above

In this method, you convert part of your savings into an annuity. An insurance company pays you a fixed income for life. This removes the need to manage withdrawals.

For example, you invest a lump sum and receive a monthly income. This income continues regardless of market conditions. It helps cover basic expenses like food, rent, and medical needs.

This strategy provides strong income stability. It reduces financial stress in later years. It works best when you want guaranteed cash flow.

Risks:

- Limited flexibility after purchase

- Lower returns compared to market investments

- Inflation can reduce purchasing power

Each strategy offers a different balance of stability and flexibility. You can also combine them to match your needs at different stages.

How to choose from the different retirement withdrawal strategies?

Choosing a withdrawal plan becomes easier when you follow clear steps. Each step helps you match your income with your real needs. Take it one step at a time and keep it simple.

Step 1: Calculate Your Monthly Spending

Start with your basic expenses. Include rent, food, bills, and medical costs. Then add flexible expenses like travel and hobbies. This gives you a clear monthly target.

If your spending is stable, you can choose a fixed income strategy. If it changes often, a flexible approach will work better.

Step 2: Check Your Income Sources

List all income streams. This can include pension, rental income, or part-time work. Some people rely only on savings, while others have support.

If you already have a steady income, you can take more risks. If not, you should focus on stable withdrawal methods.

Step 3: Understand Your Risk Comfort

Think about how you react to market drops. Some people stay calm, while others feel stressed. Your comfort level should guide your choice.

If you prefer peace of mind, choose stable income strategies. If you can handle changes, flexible strategies may help your money last longer.

Step 4: Estimate How Long You Need the Money

Think about your retirement length. Your retirement withdrawal strategies should depend on how long you need money. A longer retirement needs a lower withdrawal rate. This helps protect your savings over time.

If your timeline is shorter, you can withdraw slightly more. Still, you need to stay careful with large withdrawals.

Step 5: Match Strategy to Your Needs

Now connect everything.

- Stable expenses + low risk → fixed income methods

- Flexible spending + higher risk → dynamic methods

You can also mix strategies. For example, use an annuity for basic needs and a flexible plan for extra spending.

Step 6: Review Your Plan Every Year

Your needs will change over time. Markets will also move up and down. Review your withdrawals once a year.

Make small changes if needed. This keeps your plan steady and reduces long-term risk.

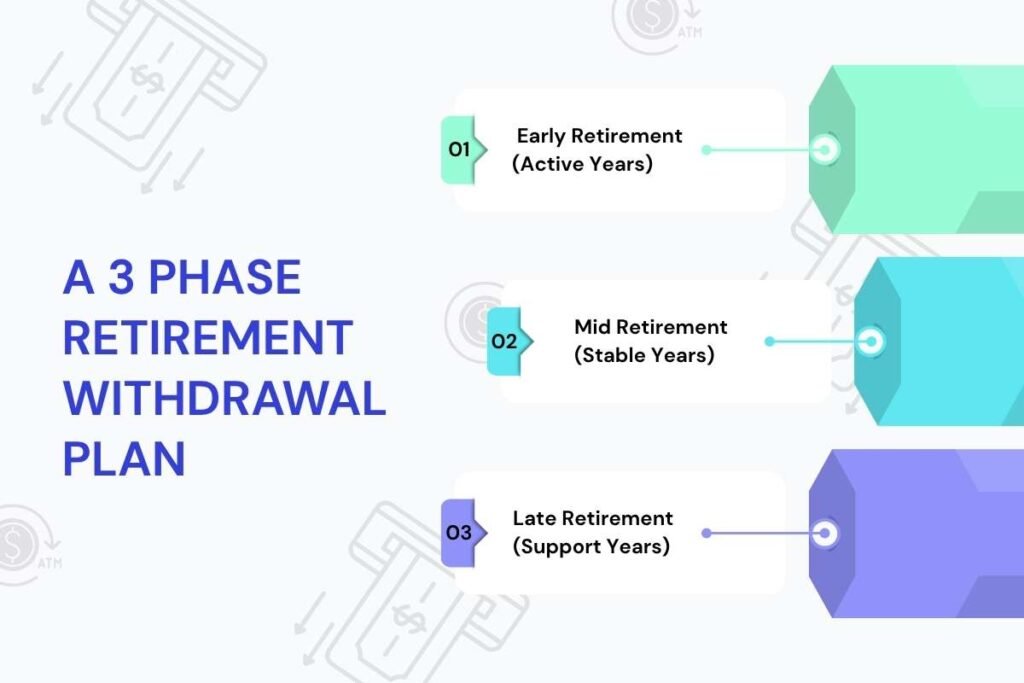

A 3 Phase Retirement Withdrawal Plan

A simple way to plan retirement withdrawal strategies is to break your retirement into three phases. Each phase has a different goal. Your withdrawals should adjust to your needs and lifestyle.

Phase 1: Early Retirement (Active Years)

This phase usually starts right after you retire. You stay active and spend more on travel, hobbies, and experiences. Your withdrawals are higher in this stage.

For example, if you have ₹1 crore, you may withdraw around 5 to 6 % each year. This supports a more active lifestyle. You can combine a flexible strategy with some cash reserves to handle market swings.

The focus here is enjoyment with control. You spend more, but still keep an eye on your portfolio.

Phase 2: Mid Retirement (Stable Years)

In this phase, your lifestyle becomes more settled. Travel slows down, and daily routines become simple. Your expenses become stable and predictable.

You can reduce withdrawals to around 3 to 4 %. This helps your savings last longer. A fixed %age or balanced strategy works well here.

The goal is stability. You maintain your lifestyle without putting too much pressure on your savings.

Phase 3: Late Retirement (Support Years)

This phase focuses on care and security. Health costs increase, and you may need support at home. Spending rises again, but in a different way.

You may rely more on steady income sources. This can include annuities, pensions, or low-risk investments. Withdrawals from savings may reduce, but total expenses can still rise.

The goal here is certainty. You ensure that your basic needs are always covered.

This three-phase approach keeps your plan realistic. It matches your withdrawals with how your life changes over time.

Conclusion:

Your retirement withdrawal strategies should grow with you. Spending will rise, fall, and rise again over time. A fixed plan may not keep up with these changes.

Focus on matching your income with your needs. Use stable income for essentials and flexible withdrawals for lifestyle goals. This gives both safety and freedom.

Review your plan every year. Small changes can protect your savings and improve your income flow. The right retirement withdrawal strategies help your money last longer and support you at every stage.

People also ask:

1. Is the 4% rule still safe?

It can work, but it is not perfect. Market conditions, inflation, and longer life spans can affect it. Many people now use it as a starting point and adjust based on their situation.

2. Should I spend less in a bear market?

Yes, reducing spending during market drops can protect your savings. Even a small cut can help your portfolio recover faster. Flexible strategies work well in these periods.

3. When should I start taking Social Security?

It depends on your needs and health. Starting early gives you income sooner, but at a lower amount. Waiting increases your monthly benefit.