Learn how to make your retirement income last with smarter retirement cash flow planning that protects against inflation, market shocks, and longevity risk. This guide explains why most plans quietly fail, how to build a realistic monthly budget, structure reliable income sources, optimize withdrawals and taxes, and stress-test your strategy. Instead of focusing only on savings, you’ll discover a practical system designed to keep cash flowing securely throughout retirement.

Often, retirement cash flow planning is treated as a simple budgeting exercise. It is a survival system for your financial independence, in fact. Most retirees think about “how much they saved” and don’t think about “how money flows out over time.” This is where most plans die a slow death.

The real question isn’t whether you have enough money today. But if your retirement income can withstand inflation, market downturns, healthcare shocks, and longer lifespans. This guide distils retirement cash flow planning into a systemised, stress-tested system that shows you where most plans break, and how to fix them before retirement begins.

Why do most retirement cash flow planning fail quietly?

Most retirement cash flow planning doesn’t work, but not because people don’t save enough; it works in the background, slowly eroding income through withdrawal sequencing and inflexible rules. Sequence-of-returns risk involves drawing the same dollar amount in early bad-market years, forcing portfolio sales at low prices, magnifying losses, and diminishing future income capacity. Static withdrawal assumptions, fixed percentages or inflation-only increases, ignore market volatility, longevity variance, and spending shocks. So plans look good on paper, but leak value in practice.

Hidden leakage points are excessive fees, tax-inefficient withdrawals, poor timing of annuitization, treating required minimum distributions as spending, and not rebalancing or using buffer assets (cash, bonds) to tide over downturns. Small under-adjustments compounded over decades transform a “sustainable” plan into one that quietly bleeds real resources.

Move away from single-number outcomes to adaptive withdrawal frameworks, guardrails (spend bands, buffers, dynamic rules), and tax-aware sequencing to preserve purchasing power and reduce silent failure. Retirement cash flow planning is about sequencing, not just savings targets.

Your Real Monthly Retirement Budget:

Most retirees overestimate how tidy their monthly budget will be. The “guesswork” version omits inflation-adjusted essentials, rising medical costs, and early-retirement lifestyle inflation. Build a real monthly retirement budget by mapping expenses, not averaging them.

- Split expenses: fixed (housing, insurance, debt), essential variable (food, utilities, basic transport), discretionary (travel, hobbies).

- Adjust for escalation: apply realistic inflation rates to essentials (use 2–4% for basics, 4–7% for healthcare).

- Identify silent expense creep: one-off lifestyle upgrades, subscription drift, family support, and health-related add-ons that gradually shift categories from discretionary to essential.

- Create a cash-flow model: monthly baseline = fixed + essential variable (inflation-adjusted); add a rolling 12-month discretionary envelope with smoothing rules (cap increases, pause triggers).

- Stress-test with shocks: simulate a 10–30% jump in medical outlays and a 2–3 year higher discretionary phase (travel, hobbies) to see buffer needs.

Result: a precision monthly model that shows true income requirements, buffer size (liquidity for 2–5 years), and when/if withdrawal rules must tighten, making retirement cash flow planning actionable rather than hopeful.

Cash Flow Sources: Building a Reliable Income Stack

A reliable retirement income stack is layered, not lumped together. The goal is to allocate each layer to a different level of spending risk to maintain cash flow stability without having to sell at the wrong time.

- Core guaranteed income covers essentials first, including pension-like payments, annuity income, and Social Security equivalent benefits.

- Investment income adds a second layer through dividends, bond interest, and other predictable portfolio income.

- Flexible liquidation is the backstop, using equity withdrawals only when needed and preferably in a planned, tax-aware way.

This architecture matters because it reduces pressure on investments during market stress. Instead of relying on one source to do it all, the system provides a guaranteed income to meet the basic needs, an investment income to fund lifestyle spending, and liquid assets to cover variability. This provides for a more consistent monthly cash flow and lessens the chance that you will need to sell growth assets at an inopportune time.

Smart Withdrawal Strategy That Survives Market Cycles:

Here’s a simple list of market-resilient withdrawal strategies for Retirement cash flow planning:

- Guardrails approach. Start with a planned withdrawal rate, then raise or cut spending when the portfolio moves outside set limits. This helps prevent overspending in weak markets.

- Flexible inflation adjustment. Instead of increasing withdrawals every year no matter what, ties raises to portfolio performance and inflation conditions.

- Core-and-discretionary split. Use guaranteed income and bond/dividend income for essentials, and fund lifestyle spending from flexible withdrawals.

- Reduce withdrawals in downturns. In a down market, cut non-essential spending or delay big purchases to avoid selling too many assets at low prices.

- Systematic withdrawal plan. Take a regular amount, but review and adjust it periodically instead of treating it as fixed forever.

- Annual recheck. Revisit cash flow, income sources, and market conditions once a year so the plan stays aligned with reality.

Inflation + Longevity: The Silent Cash Flow Killer

Inflation and longevity quietly break retirement cash flow planning by shrinking what each dollar buys and by extending the number of years money must last. Even a modest inflation rate can cut purchasing power sharply over 20–30 years, and the longer someone lives, the more that loss compounds into an income gap.

Simple version

- Real purchasing power decay: A fixed income buys less every year, so the same monthly withdrawal covers fewer essentials over time.

- Why average inflation misleads: ”Average” inflation hides the fact that real retiree costs, especially healthcare, can rise faster than the headline number.

- Longevity as a multiplier: Living longer doesn’t just add more years; it multiplies the effect of inflation because the higher costs repeat for a longer period.

Why it matters

A retirement plan can look stable on paper and still fail in real life if withdrawals are not adjusted for rising costs and a longer lifespan. That is why Retirement cash flow planning needs inflation-aware withdrawals, not flat-dollar assumptions.

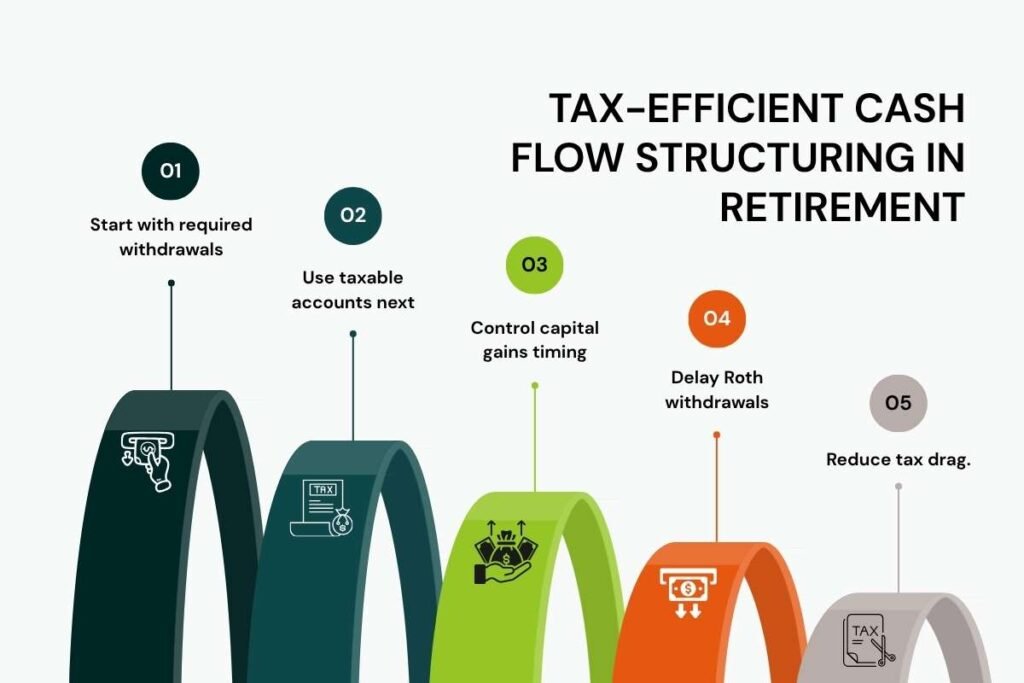

Tax-Efficient Cash Flow Structuring in Retirement:

Tax-efficient cash flow structuring in retirement is about choosing the right withdrawal order so you keep more of what you earn and reduce tax drag over time. The usual logic is: cover required withdrawals first, then use taxable income sources and gains carefully, and leave Roth assets for last when possible.

Simple structure

- Start with required withdrawals. If you have RMDs, take them first because they are mandatory and usually taxed as ordinary income.

- Use taxable accounts next. Interest and dividends can fund spending, and long-term capital gains are often taxed lower than ordinary income.

- Control capital gains timing. Sell appreciated assets in years when your income is lower so gains may be taxed more lightly.

- Delay Roth withdrawals. Roth money is often best saved for last because qualified withdrawals are tax-free, and Roth accounts do not have RMDs.

- Reduce tax drag. A tax-aware sequence can help keep more income invested and improve long-term retirement cash flow.

Stress Testing Your Retirement Income Plan:

When stress-testing a retirement plan, you aren’t looking at averages. You are looking at worst-case combinations. Here are three critical failure scenarios to simulate before you retire.

1. Market Crash in Year One (Sequence of Returns Risk)

- The Shock: A $25\%$ market drop right as you retire, paired with inflation-adjusted withdrawals.

- The Failure: You lock in heavy losses early by selling depressed assets to fund living expenses. This permanently damages your portfolio’s compounding engine, potentially running it dry 10 years too early.

2. High Inflation Decade

- The Shock: Inflation averages $6-8\%$ for 10 straight years (similar to the 1970s).

- The Failure: To maintain your purchasing power, your annual withdrawals must nearly double in a decade. If your portfolio is too heavily weighted in fixed income (bonds/cash), its real value will rapidly erode.

3. Medical Expense Shock

- The Shock: An unexpected, out-of-pocket long-term care event costing $\$100,000+$ annually.

- The Failure: Forcing massive, unplanned portfolio liquidations. This can spike your taxable income, pushing you into higher tax brackets and triggering steep Medicare premium surcharges (IRMAA).

- The Fix: Shift from “average return” thinking to “buffer asset” thinking. Maintain a 3-to-5-year cash/short-term bond bucket to avoid selling stocks during these exact crises.

Building a Future-Proof Income System:

A strong retirement income plan is more like an automatic distribution plan than a savings account. The shift from net-worth growth to strategic retirement cash flow planning is the key to creating a future-proof framework.

1. Diversification of Income Streams

Layer your cash flow into three distinct tiers to balance stability and growth:

- Guaranteed Base: Social Security, pensions, or annuities to cover fixed, non-negotiable living expenses.

- Variable Growth: Dividend-paying stocks, ETFs, and real estate to combat long-term inflation.

- The Buffer: 2–3 years of cash equivalents (CDs, money market funds) to draw from when markets decline.

2. The Annual Recalibration Method

Every December, run a dynamic guardrail assessment. If your portfolio falls below a specific threshold, automatically freeze your inflation adjustment for the next year. If markets rally, refill your cash buffer.

3. Cash Flow Sustainability Checklist

Before executing withdrawals each year, verify these three metrics:

- Safe Withdrawal Rate: Is your current withdrawal rate still under 4.5% of the total portfolio?

- Tax Bracket Optimization: Are you blending traditional IRA, Roth, and brokerage withdrawals to minimize your tax hit?

- RMD Readiness: Are you prepared for Required Minimum Distributions to avoid heavy penalties?

Conclusion:

Often treated as a simple budgeting exercise, true retirement cash flow planning is actually a survival system for your financial independence. It shifts your focus from a static savings target to a dynamic, weather-tested distribution framework.

By layering your income stack, installing flexible guardrails, and shifting from “average return” thinking to “buffer asset” safety, you prevent sequence risk and inflation from quietly bleeding your nest egg dry.

Take control of your financial future today. Review your distribution sequence, map your real monthly expenses, and build an adaptable framework that guarantees absolute peace of mind for decades to come.

FAQ:

1. How to manage cash flow in retirement?

By diversifying assets and carefully planning withdrawals from various income sources like pensions and investments.

2. What is the 30 30 30 10 rule for retirement?

The rule is a disciplined way to manage your finances. It suggests that you should allocate 30% of your income to living expenses, next 30% to your retirement savings for a peaceful and secure future, another 30% to investments, and the remaining 10% to unforeseen financial situations that can arise anytime.

3. What are the 5 P’s of retirement?

The five pillars of retirement planning are tax, investment, income, healthcare, and estate. They form the foundation of a strong retirement strategy.

4. What is the 3 3 3 rule for money?

In finance and personal wealth building, the “3-3-3 rule” generally refers to one of three different frameworks depending on your goal.

5. What is Warren Buffett’s golden rule?

Warren Buffett’s famous golden rule of investing is: