The first step in retirement planning for couples is to get on the same page about your future together. It is not just about savings or investment returns. This guide explores how couples can navigate differing retirement timelines, spending styles, inflation risks, healthcare expenses, and emotional anticipations by implementing a shared decision-making system. You’ll learn practical stress-testing techniques, long-range financial planning strategies, and a retirement checklist to help both partners stay financially ready, emotionally connected, and resilient for the next 25-30 years.

When you and your partner start talking about retirement planning for couples, the real question is not “how much have we saved?” but “are we really on the same page for the next 25–30 years?”

Most couples assume that retirement is a shared destination. In fact, it is two timelines, two ways of spending, and two emotional expectations that collide over time. One partner may want travel and activity, the other may want stability and low-risk living.

This guide simplifies retirement planning for couples into a system that covers financial preparedness, emotional compatibility, and real-world experiences that are often left out.

The hidden gap in retirement planning for couples:

Most couples assume retirement planning is a joint, linear journey, save together, retire together, and spend together. In reality, most couples experience asynchronous retirement: one retires earlier, one keeps working, and life does not neatly adjust to the new phase.

This creates a hidden gap:

- One partner retires, and the other is still earning.

- Household spending patterns stay the same or even rise because the retired partner has more free time.

- Health needs, energy, and lifestyle change at different speeds for each partner.

Financially, this means you have two separate timelines trying to run on one household budget. This builds up invisible pressure over time: the working partner may feel like they are “carrying” the finances, while the retired partner may feel guilty or defensive about spending. Unspoken, small frustrations can become:

- Unequal contribution narratives (“I’m paying for everything now”).

- Silent resentment about what is “necessary” vs “luxury” spending.

- Early, unplanned withdrawals from long-term savings to “bridge the gap.”

This is not a new product but a new mental model: from “shared savings” to “shared system thinking.” Couples don’t view themselves as one big pot of money, but rather as two financial profiles sharing a single household system. Each has its own income path, retirement date, risk needs, and health trajectory, all coordinated through joint rules for cash flow, investing, and withdrawals.

This shift keeps the conversation focused on designing the system together, not judging each other’s choices. What part of this feels most relevant to your situation: the timing gap, the spending friction, or the health‑and‑energy differences?

Why most couples misalign financially without realizing it?

Misalignment in money doesn’t suddenly appear at 60; it quietly builds over 20–30 years. Most couples talk about goals, but not the actual system behind their money. Over time, they drift into separate financial realities without noticing.

Common triggers:

- One partner “takes over” finances, the other checks out.

- Different risk styles: one loves equity growth, the other prefers fixed income safety.

- Different emotional meanings of “security” (for one, it’s cash in the bank, for the other, it’s investments).

- Only one partner truly knows their total net worth and how it’s changing.

The real danger is in the mind. People create a personal “mental retirement picture” based on assumptions, fears, and expectations. Those pictures often clash with each other, and with the real numbers. Once couples get serious about retirement planning.

A strong retirement planning for couples approach is simple:

- Full visibility of net worth for both partners

- A joint discussion about risk tolerance and investment mix

- A shared view on how and when to withdraw money in retirement

Without this, couples usually discover gaps only when one of them retires, and by then, the options are narrower, and the emotions are louder.

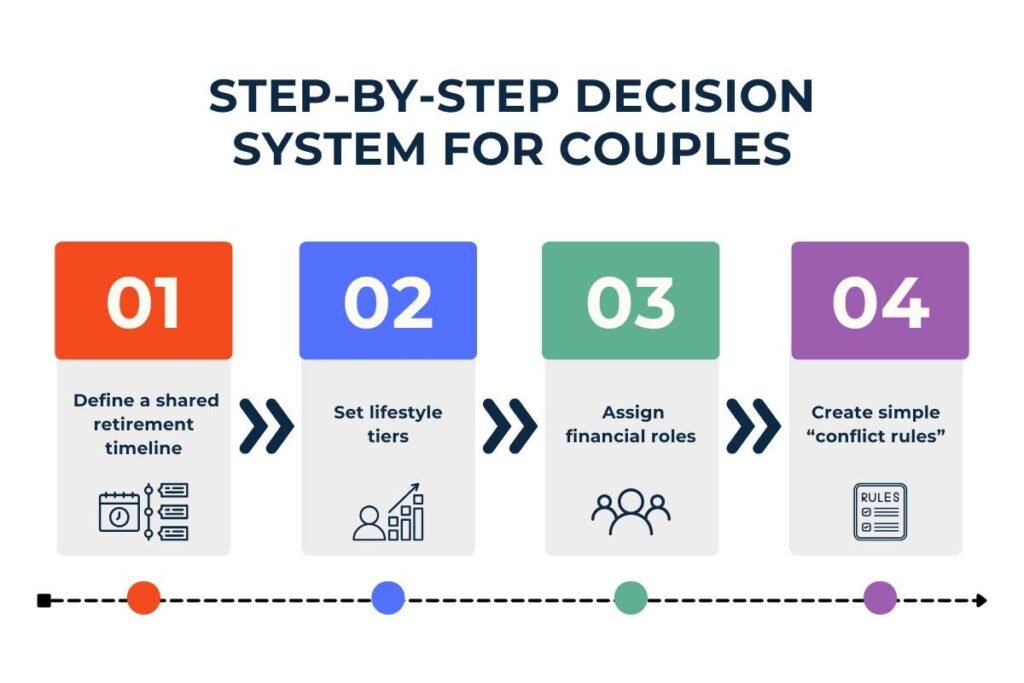

Here is a step-by-step decision system for couples:

Searching the web for retirement planning decision frameworks for couples. Most advice on retirement planning for couples is about what to do, not how to decide as a couple. A simple, repeatable decision system helps manage emotions and maintain consistency over time.

Step 1: Define a shared retirement timeline

- Will you stop working at the same age or at different ages?

- Is there a partial retirement phase (reduced hours, consulting, side income)?

Write this down as your “household retirement calendar.”

Step 2: Set lifestyle tiers

- Minimum survival lifestyle: basics only, no extras.

- Comfortable lifestyle: your realistic, preferred standard of living.

- Aspirational lifestyle: travel, hobbies, upgrades if markets and health cooperate.

This helps you adjust spending quickly when markets or income change.

Step 3: Assign financial roles

- Who tracks investments and reports back monthly or quarterly?

- Who manages day-to-day spending and bills?

- What amount requires joint approval (for example, any purchase above a set limit)?

Step 4: Create simple “conflict rules”

- How will you pause and review if you disagree on a purchase?

- Clear rules for when you can tap long-term savings.

- A process to adjust investment risk if one partner feels unsafe.

This turns retirement planning for couples from emotional guesswork into a shared system you both understand and control.

Stress-test scenarios every couple must plan for:

I’m looking for information on retirement stress testing for couples. The usual advice about retirement is based on the quiet assumption that “nothing major goes wrong.” But real life doesn’t cooperate. Stress-testing, not just optimistic projections, is essential to strong retirement planning for couples.

Key scenarios to plan for:

- A market crash in the first years of retirement (sequence-of-returns risk)

- One spouse’s early death and its impact on income, pensions, and expenses

- Long-term medical or caregiving dependency for either partner

- Housing shocks: rent hikes, forced sale, or expensive relocation

- Currency or high-inflation shocks if income and expenses are in different currencies

For each scenario, couples should answer three simple questions:

- Will the remaining income and assets still sustain both partners’ basic lifestyle?

- Who becomes financially dependent on whom, and for how long?

- Which assets are actually liquid and usable in a crisis (not locked up or highly volatile)?

A practical rule: simulate at least three different “bad but plausible” stress cases before retiring. This can be as simple as using a spreadsheet or planner tool to plug in:

- A 30–40% portfolio drop

- The loss of one pension or income stream

- A major rise in medical or housing costs

This turns retirement planning for couples from hope-based to resilience-based, so shocks feel like rehearsed events, not total surprises.

Inflation, longevity & “age 80+ risk” explained:

The biggest blind spot for couples in retirement planning is not market returns, but how long both partners might actually live. Many plans assume 20 years post-retirement in silence, but global and Indian data now show that retirees may need to fund 25-30+ years, especially for women and healthier non-smokers.

After age 70, two forces hit at once:

- Medical costs and health insurance premiums tend to rise faster than general inflation, often becoming the largest retirement expense.

- The ability and desire to earn side income usually drops for both partners, which means less flexibility to “work your way out” of a shortfall.

The real “age 80+ risk” is a long tail of expenses:

- Ongoing medical inflation and out-of-pocket health spending in older age.

- Possible assisted living, home care, or full-time caregiving needs that can last many years.

A robust retirement planning for couples strategy should:

- Assume at least 30 years of withdrawals, not 20, based on longevity risk research.

- Build in a rising healthcare allocation every 5–7 years, reflecting faster healthcare inflation versus general prices.

The plan is built on the most probable scenario, which is a long life with increasing medical costs, not a short, “average” retirement.

This is a must-have retirement planning checklist for couples:

A high-value retirement planning for couples checklist should keep money, lifestyle, and risk on the same page. Use this as a quick “completion tracker,” not a theory lesson.

Financial checklist

- Joint net worth transparency completed (both partners see the full picture).

- All retirement income sources mapped: pensions, EPF/401(k), NPS, annuities, rental, SWPs.

- Inflation-adjusted projections created for at least 25–30 years.

- An emergency fund kept outside the retirement corpus.

- Tax-efficiency strategy reviewed (withdrawal order, account types, deductions).

Lifestyle checklist

- Retirement age alignment discussed and written down.

- Housing plan finalized: stay, downsize, or relocate.

- Travel versus stability preferences aligned (how much, how often, for how long).

- Daily routine expectations discussed: work, hobbies, caregiving, and family time.

Risk checklist

- Medical insurance coverage reviewed for both partners post-retirement.

- Long-term care or caregiving plan included (insurance, savings, or family support).

- Market crash / sequence-risk scenario tested on the plan.

- Survivor income planning completed (pensions, Social Security, insurance, assets).

Key things to keep in mind before you retire:

Before you finish planning your retirement as a couple, make sure you’re both on the same page. It is not just about the numbers, but about how you want to live, make decisions, and react to crises. Many plans fail because the math is wrong, but everyone secretly has a different picture of retirement.

Retirement is not a one-time event but a long-term system that needs to be reviewed annually and adjusted as health, markets, and priorities change. Both partners need to agree on:

- Lifestyle expectations (pace of life, travel, work after retirement, daily routines).

- Decision rules for spending, investments, and withdrawals.

- Crisis scenarios (health shock, market crash, one partner’s early death) and how the plan responds.

This keeps retirement planning for couples practical, shared, and resilient, rather than a hopeful guess that unravels once the first big shock hits

Conclusion:

For couples, retirement planning isn’t just about savings. It is about aligning two lives, two timelines, and two notions of “security” into one shared system. As this guide has revealed, the real danger is not in how much you have. But how well you and your partner have articulated your timeline, lifestyle tiers, and crisis rules. Thinking of retirement as a long-term system, and regularly stress-testing market shocks, health needs, and longevity. This can get couples from hopeful guessing to a resilient, joint plan. Retirement planning for couples is less about money and more about designing the next 25-30 years together, on the same page, when both partners own the numbers, the conflicts, and the trade-offs.

FAQ:

1. What is the 50/30/20 rule for couples?

The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals.

2. What is the 30-30-30-10 rule for retirement?

The rule is a disciplined way to manage your finances. It suggests that you should allocate 30% of your income to living expenses, next 30% to your retirement savings for a peaceful and secure future, another 30% to investments, and the remaining 10% to unforeseen financial situations that can arise anytime.

3. What is the biggest mistake most people make regarding retirement?

The most significant retirement mistake is failing to plan and track a realistic monthly budget, which often leads to either overspending and depleting funds too early or underspending out of fear and missing out on the golden years.

4. What is the 3-6-9 rule of money?

Those general saving targets are often called the “3-6-9 rule”: savings of 3, 6, or 9 months of take-home pay.

5. What are the four behaviors that cause 90% of all divorces?

According to Dr. John Gottman’s research, the four behaviors that can predict divorce with over 90% accuracy are criticism, contempt, defensiveness, and stonewalling.